The tech hardware supply chain US-China decoupling is an element of the current geopolitical competition. Nevertheless organizations in the supply chain may still take advantage of the reshaping of electronics production that the decoupling has caused. This blog article is based on RCD Advisors Insights post and its expertise. Published by EPCI.eu under RCD permission.

In late May 2023, China retaliated at the long string of US trade restrictions by banning Micron’s memory chips from critical domestic infrastructure projects.

It’s the latest salvo in an escalating geopolitical competition. Unfortunately, the Tech hardware supply chain is on the front lines. But, despite the crossfire, there may be opportunities for supply chain organizations to capitalize on the massive reshuffling of electronics manufacturing caused by this decoupling.

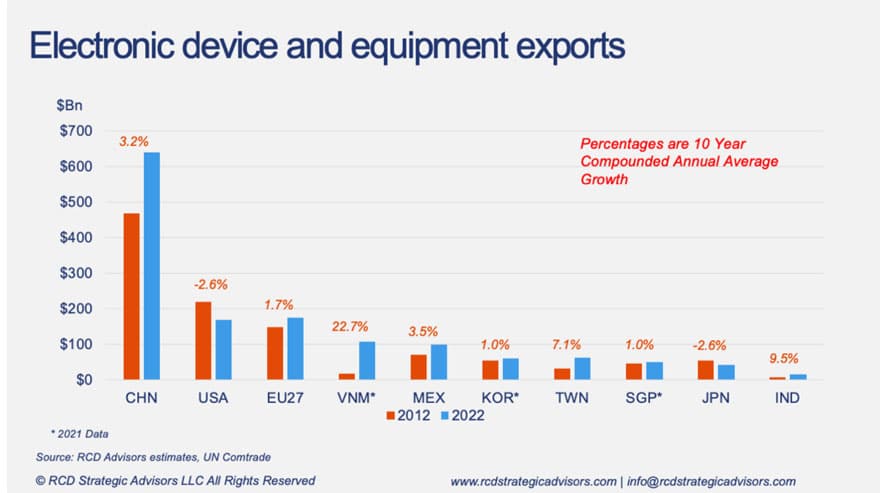

Today, China manufactures approximately 50% of all electronic devices and equipment. China has an even more significant production share in some parts of the Tech hardware supply chain.

The country has benefited from twenty years of development and over $145Bn of cumulative foreign investment to reach this dominating position. Rebuilding this electronic manufacturing network in other regions will not be easy.

China also consumes almost one-third of global electronics value within its borders. It is a significant portion of the $2.4Trn Tech hardware device and equipment market. But it is insufficient to support all the electronic manufacturing capacity already installed within China’s borders.

At least for Tech hardware, China’s turn towards self-sufficiency and a more consumption-based economy won’t be easy either.

The geopolitical drama impacting Tech hardware over the next decade comes down to two questions: How fast do foreign investment and capability develop in emerging manufacturing regions?

And, how quickly can China jump-start domestic consumer spending to match its manufacturing capacity? Below are some considerations for Tech hardware component suppliers.

China’s Consumers Won’t Pick Up the Slack

Although growing, Chinese consumers, in total, spend far less on electronics than in the US.

China’s total electronics consumption could grow faster if business and government investment spending increased. But these investments can’t continue unbounded from consumer demand unless there is continued export growth. Unfortunately, exports are under pressure from trade policy. So business and government investment spending is unlikely to pick up the slack either.

China for China and Friends

Does it make sense for Chinese companies restricted from operating in the US (or Europe or Japan) to maintain an overseas presence? China minus the West may become a rational business decision for these companies. Instead of focusing on advanced economies, Chinese nationals may be better off focusing on the domestic market and the willing “Belts and Road” emerging economies. Huawei has been able to pivot to Asia, the Middle East, and Africa. Other suppliers like BKK, ZTE, and Haier have also redirected to these emerging regions. It is only a matter of time before the rest of their supply chains follow.

“Plus-one” only?

In recent years, China’s emphasis on self-sufficiency has incentivized the local Tech hardware industry to use domestic component suppliers over foreign nationals. The origins of this effort can be traced to the Made-in-China Policy initiative issued in 2015. But this effort raises an interesting question. Does it even make sense for foreign component suppliers to manufacture in China if they can’t serve China?

The answer depends on an organization’s competitive advantage and its trade restrictions. Companies like Tesla or Apple have rarefied global reach and appeal. Companies like Nvidia have developed a considerable lead in machine learning processors. Chinese domestic sources cannot replace these companies. At least, not yet.

But most component sectors (connectors, passives, PCBs, discretes) are more competitive with multiple capable suppliers. So, there is a legitimate need to re-evaluate where manufacturing should be in these sectors. “China plus one” is the cliche. The idea is for foreign manufacturers to produce in China for the domestic market and have an alternative location to reduce supply chain risks and bypass trade barriers. But if domestic competitors in China enjoy privileged investments and preferential treatment, a “plus one” only manufacturing strategy is a plausible option for foreign firms.

New Destinations for Tech Hardware Manufacturing

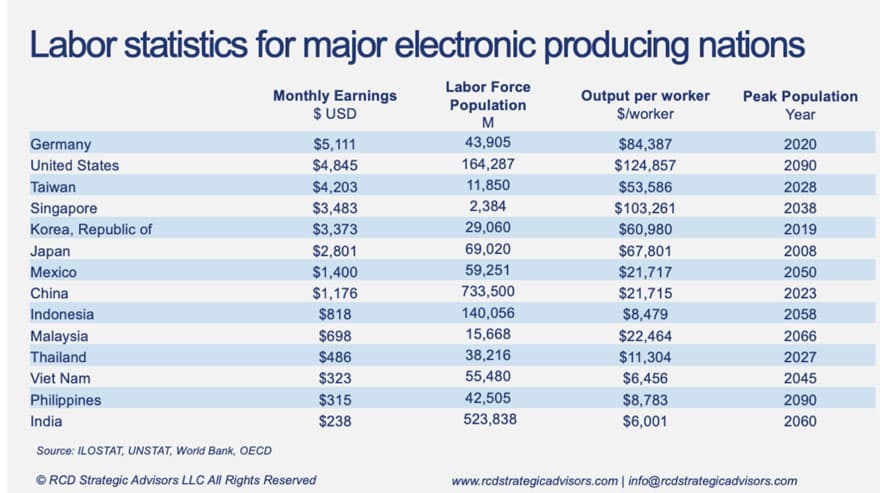

It is well known that no country has benefited more from China’s decoupling efforts than Vietnam. Like other South Asian countries, Vietnam has low labor costs and incentives to attract foreign investment. But Vietnam has a smaller population (comparatively) and underdeveloped infrastructure.

Can Vietnam parlay the growth in manufacturing to develop the workforce required to move up the value chain into semiconductors and electronic design? It’s possible, but the country may be hitting a ceiling. Since 2013, Vietnam has seen electronics industry-specific investment inflows of $28Bn (link).

The first few waves of the supply chain have already established manufacturing locations in the country. Vietnam will have to develop its workforce quickly to move up the smile curve because the demographic advantage will disappear in the next fifteen years.

Vietnam fits perfectly into the “China plus one” theme. Vietnam is not a threat to overtake China in electronic manufacturing supply chains. The domestic market is too small (It will never grow larger than Japan’s value today), and there are few homegrown suppliers. But it is large enough to offer a “plus one” safety valve.

India also has the potential to become a dominant manufacturing hub for tech hardware. Despite challenges such as lacking infrastructure and bureaucratic hurdles, recent industry commitments suggest India’s favorable demographics and emerging market make it an attractive option. In addition, the government’s efforts to attract manufacturing through incentives and reduced protectionist policies also contribute to India’s potential. However, there will be growing pains (such as incentivizing portions of the labor force to migrate from rural areas to industrial hubs).

India is still in the early stages of this development. According to Invest India, a government agency, foreign direct investment in electronics has accumulated to $3.5Bn since 2000. Nevertheless, India is a legitimate threat to overtake China as a manufacturing hub. Part of the attractiveness of India is that there is already an established domestic electronics supply base. It provides a springboard for developing a completely independent ecosystem for exports to the rest of the world. As a result, manufacturing in India is a long-term bet on complete decoupling.

Other South East Asia countries could also become viable options, and some have strategically focused on particular subsectors. For example, Thailand has historically been a manufacturing hub for hard disk drives and optical components industries. Likewise, Indonesia has focused its incentives and resources on electric vehicle manufacturing. Malaysia has developed a formidable ecosystem in backend semiconductor assembly.

This focused approach may work for these countries. But they are constraining and less attractive to broad-line component vendors looking to move out of China. Moreover, none of these countries have the demographics to match India’s or have grown as rapidly to take advantage of China’s decoupling as Vietnam.

In the past, South/Central America, Eastern Europe, and African countries were considered ideal locations for electronic assembly expansion due to their proximity to end markets. However, electronic assemblies have low shipping costs. Proximity is not crucial unless there is an engineering design advantage. With Europe and the US starting to restore wafer fabrication, there is potential for certain parts of the supply chain (such as backend semiconductor packaging) to relocate to these regions. Manufacturing in one of these regions is a bet on reshoring.

Opportunities in a Reshuffled Supply Chain

For Chinese domestic suppliers, the government’s turn towards self-sufficiency has brought immediate benefits. It is an attractive opportunity that will offset increasingly hostile trade restrictions.

However, with a focus on self-sufficiency and trade barriers, Chinese suppliers face an increasingly complex environment for outbound investments. Much of this complexity stems from the National Development and Reform Commission (NDRC), which in 2017 announced new rules for controlling outbound investments. The new rules encouraged some investments (particularly in countries under the Belts and Roads umbrella). But it also provided more oversight and restrictions for investments in other industries. As a result, many Chinese component makers may be restrained from making foreign investments in the future, putting them at a labor disadvantage.

In areas where Chinese component suppliers dominate the market, such as PCBs and some passive component segments, there is an opportunity for foreign firms to gain market share in high-volume device applications by investing in Vietnam or India. It may be a small consolation for foreign companies who may eventually have to cede the Chinese market. But it is a worthwhile bet on where customers will be.

Component makers primarily serving low-volume and high-mix markets in Europe, Japan, or the US, have different priorities. They are unlikely to benefit from increases in market share in the high-volume smartphone or PC supply chain. These firms should consider expanding to countries like Vietnam or India to access quality, low-cost labor to remain competitive.

It may be more prudent for these companies to follow the lead of equipment manufacturers who have already established themselves in these emerging regions. For Vietnam, the time is now because much of the high-volume supply chain is transitioning. For India, that time may not be too far away.

The Tech hardware supply chain is undergoing a massive geographic reshuffling. As with any change, there are opportunities and threats. RCD Advisors’ mission is to help organizations navigate and capitalize on these changes. If you find these posts insightful, subscribe to have them delivered to your email. If you want to learn more about the consulting practice, contact info@rcdadvisors.com.